Held by Hon’ble High Court of Bombay

In the matter of Shantanu Sanjay Hundekari Vs. Union of India(WRIT PETITION (L) NO. 30198 OF 2023)

The Petitioner is an employee of a Company M/s MLIPL, which is appointed as steamer agent of M/s Maersk. The petitioner was assisting M/s MLIPL against GST Compliance and was holding power of attorney to represent before tax authority on behalf of M/s Maersk. During the course of investigation, it was alleged that M/s Maersk has availed ineligible ITC and has made wrongful distribution of ITC. A SCN was issued to the petitioner asking to pay INR 1561 Crores equivalent to the tax alleged to be evaded by M/s. Maersk. Notice was issued under section 74 of CGST Act invoking Section 122(1A) and section 137 of CGST Act.

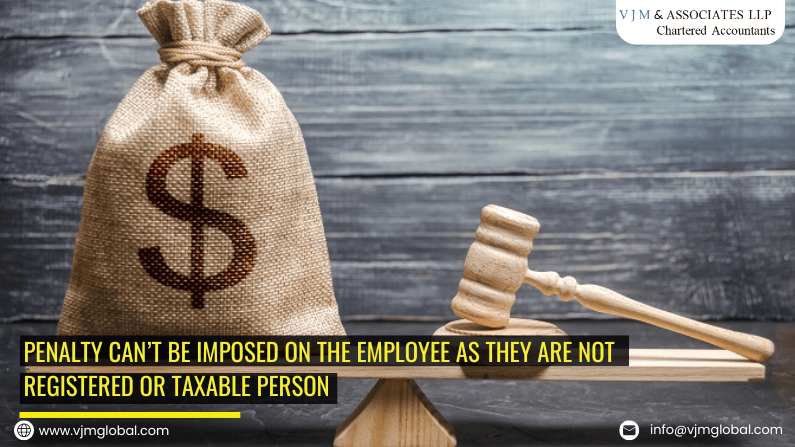

Hon’ble High Court anaylsised that Provisions of Section 122(1A) can be invoked against a taxable person who would be in a legal position, to retain the benefit of tax, and at whose instance, such transaction is conducted. In the given case, the petitioner is merely an employee and cannot fall within the purview of the said provision, as the petitioner cannot be a ‘taxable’ or a ‘registered person’ within the meaning and purview of the CGST Act so as to retain such benefits as the provision ordains. Further, Show cause notice is issued under Section 74 of CGST Act. Section 74 is not a penal provision, whereas Section 137 falls under Chapter XIX which provides for ‘offences and penalties’. Therefore, as to how such penal provision in Section 137 could be foisted against the petitioner, when the show cause notice is itself a demand cum show cause notice. Therefore, impugned show cause notice is rendered bad and illegal, deserving it to be quashed and set aside.

1. Brief facts of the case

- In the given case, the petitioner is an individual who is an employee of the Company M/s. Maersk Line India Pvt. Ltd. (“MLIPL”).

- M/s MLIPL is a company having its principal place of business at Mumbai.

- The petitioner was working as a Taxation Manager with M/s MLIPL. The Company was appointed as Steamer agent of Maersk A/S (“Maersk”), a company incorporated in Demark.

- M/s Maersk is engaged in the shipping business involving containerized transportation of goods, through vessels across the globe.

- The petitioner, as a Taxation Manager, rendered assistance to M/s Maersk in its compliance with taxation laws including the GST.

- The petitioner also holds power of attorney to represent Maersk before the Tax Authorities. However, the petitioner was not in-charge of the day-to-day business of Maersk.

- The petitioner also assisted the investigations being conducted by the tax authorities in matter of M/s Maersk such as responding to the summons, presenting evidence and furnishing a list of witnesses whose statements could be recorded.

- After such inquiry, the respondents made allegations that M/s Maersk has wrongly availed ITC of Rs.1561 crores. Further, M/s Maersk has also made a wrongful distribution of ITC.

- The Petitioners are foisted with a show cause notice under Section 74 of the Central Goods and Services Tax Act, 2017 wherein they are required to pay an amount of INR 3731 Crores towards penalty.

- Such an amount is the tax amount stated to be defaulted by their employer.

- The petitioner has challenged the demand cum show cause notice issued by DGGI. As per SCN, the petitioners are called upon to show cause as to why a penalty equivalent to the tax alleged to be evaded by M/s. Maersk should not be imposed upon the petitioners.

2. Relevant Legal Extract

Relevant legal extract of the GST law is reiterated below for ready reference:

- “Section 122. Penalty for certain offences –

….

(1-A) Any person who retains the benefit of a transaction covered under clauses (i), (ii), (vii) or clause (ix) of sub-section (1) and at whose instance such transaction is conducted, shall be liable to a penalty of an amount equivalent to the tax evaded or input tax credit availed of or passed on. ……………..”

- “Section 137. Offences by companies

(1) Where an offence committed by a person under this Act is a company, every person who, at the time the offence was committed was incharge of, and was responsible to, the company for the conduct of business of the company, as well as the company, shall be deemed to be guilty of the offence and shall be liable to be proceeded against and punished accordingly.

(2) Notwithstanding anything contained in sub-section (1), where an offence under this Act has been committed by a company and it is proved that the offence has been committed with the consent or connivance of, or is attributable to any negligence on the part of, any director, manager, secretary or other officer of the company, such director, manager, secretary or other officer shall also be deemed to be guilty of that offence and shall be liable to be proceeded against and punished accordingly.

…”

3. Contention of the Petitioner

The Petitioner has contended that:

- The petitioner has not personally availing the benefit of any ITC. Also, show cause notice does not allege that any personal benefit is achieved by the petitioner.

- Show Cause Notice is making allegations against M/s Maersk.

- However, it has incidentally invokes the provisions of Section 122(1A) and Section 137 of the CGST Act to threaten imposition of penalty on the petitioner and to initiate prosecution against the petitioner, who is an individual.

- Since no personal benefit has been availed by the petitioner therefore, invoked provisions do not apply to the petitioner.

- M/s Maersk is a foreign company which does not have any employee or fixed establishment in India.

- Accordingly, solely for the purpose of representing and acting on behalf of M/s Maersk, the petitioner was given power of Attorney.

- As per the department’s allegation, credit should have been proportionately allocated among eleven different registrations of M/s Maersk in ten States.

- The petitioner was not the decision making authority on Maersk’s businesses, and was not in-charge of or responsible for the business of M/s Maersk. The petitioner was merely representing the company before tax authority to provide factual information and data.

- All legal issues raised to the Petitioner were replied to by the petitioner as per the legal opinion obtained by M/s Maersk.

- Further, the petitioner was neither a legal expert nor had any in-depth legal understanding of GST laws or its interpretation. Thus, the role of the petitioner was essentially to assist and cooperate with the investigation authorities and provide clarification relating to distribution of input tax credit.

- The GST Council in its 38th meeting held on 18 December 2019 proposed insertion of sub-section (1A) to Section 122, to specifically address the cases of fake invoices. Provisions of Section 122(1A) was introduced with effect from 1 January, 2021.

- As per the provisions, a person shall be liable to a penalty of an amount equivalent to the tax evaded or input tax credit availed, or passed on, if he retains the benefit of certain fraudulent transactions, and when such transactions are conducted at his instance.

- In the given case, the allegation is made against the petitioner in Show Cause Notice that the petitioner has “retained the benefit of the said evasion of GST by Maersk” and at the time of evasion of tax by Maersk, the petitioner was in-charge of and responsible for Maersk’s business.

- Grounds of issuance of show cause notice to the petitioner invoking Section 122(1A) and Section 137 of the CGST Act do not apply to the petitioner, absent a suggestion that any personal benefit was availed by the Petitioner.

- Provisions of section 122(1A) of the CGST Act is not applicable as the basic ingredients primary benefit of the ITC was in any manner not availed by the petitioner.

- If it claimed that the petitioner has retained the benefit of GST evasion, and that the petitioner was in-charge of and responsible to Maersk, for the conduct of its business, there was no basis as set out to support such allegation.

4. Contention of the Respondent

The respondent contended that:

- There was responsibility fastened on the petitioner in regard to the affairs of M/sMaersk. Hence, the petitioner cannot disown his involvement in the loss of revenue.

- The petitioner had tendered statements on behalf of M/s Maersk as its power of attorney holder and as a Senior Tax Operations Manager.

- Hence, the petitioner ought to have taken responsibility for the compliance of the statutory provisions of the GST laws. In this case, there was certainly connivance of the petitioner in the evasion of tax by M/s Maersk, as the petitioner was assigned the work of compliance under GST law.

- The company is not coming forward to clear the tax dues and therefore, the show cause notice was rightly pressed against the petitioner, as the petitioner would be equally responsible for his actions, although in the capacity as a power of attorney holder.

5. Analysis by Hon’ble High Court

The Hon’ble High Court has made following analysis:

- As per show cause notice, the allegation against the petitioner is in his capacity as a Senior Tax Operations Manager of M/s Maersk.

- He is called upon to show cause as to why penalty should not be imposed upon him under Section 122(1A) of the CGST Act, 2017 where M/s Maersk had committed offences under Section 122(1)(i) of the Act.

- It is alleged that the petitioner has committed offences which led to the evasion of the GST by M/s Maersk, for the reason that the invoices raised by M/s Maersk on its supplies were not in accordance with the provisions of GST law.

- It is alleged that the benefit of the said evasion of GST was retained by the noticees (which includes the petitioner). At the time of evasion of tax by M/s Maersk, the petitioner and the other employees were in charge of, and were responsible to Maersk for the conduct of the business of Maersk.

- The petitioner and other employees were very well aware about the willful omission and commission from the tax department resulting in tax (GST) evasion by M/s Maersk. Therefore, the petitioner and such other employees had rendered themselves liable to proceedings under Section 137(1) and Section 137(2) of the CGST Act, 2017.

- The question before the Court is whether the provisions of Section 122(1-A) of the CGST Act as also Section 137(1) and 137(2) would stand attracted to issue the impugned SCN against the petitioner, who is merely an employee of MLIPL and a power of attorney of Maersk.

- Applicability of Section 122(1A) of CGST Act:

- As per Section 122(1A) is concerned, it provides that any person (who would necessarily be a taxable person), retains the benefit of the transactions covered under clauses (i), (ii), (vii) or clause (ix) of sub-section (1), and at whose instance, such transaction is conducted, “shall be liable to a penalty of an amount equal to the tax evaded or input tax credit availed of or passed on”.

- Therefore, sub-section (1-A) applies to a taxable person.

- The intention of the legislature is clear that a person who would fall within the purview of Section 122(1-A) is necessarily a taxable person and a person who retains the benefits of transactions specified in Section 122(1) of CGST Act.

- Further, Section 122(1-A) also cannot be attracted in a situation when any person does not retain the benefit of a transaction mentioned and/or it is applicable at whose instance such transactions are conducted.

- The relevant provisions show that such person can only be a taxable person who would be in a legal position, to retain the benefit of tax, and at whose instance, such transaction is conducted.

- In the absence of these basic elements being present, any show cause notice of the nature as issued, would be rendered illegal.

- In the given case, the petitioner is merely an employee and cannot fall within the purview of the said provision, as the petitioner cannot be a ‘taxable’ or a ‘registered person’ within the meaning and purview of the CGST Act so as to retain such benefits as the provision ordains.

- Hence, there was no question of invoking section 122(1-A) against the petitioner.

- Applicability of Section 137 of CGST Act

- Further, as the applicability of Section 137 of CGST Act is concerned. Section 137 concerns “Offences by Companies”. Subsection (1) provides that when an offence committed by a person under the CGST Act is a company, every person who, at the time of the offence being committed, was in charge of and was responsible, to the company for the conduct of the business of the company, as well as the company, shall be deemed to be guilty of the offence and shall be liable to be proceeded against and punished accordingly.

- How Section 137 can form part of any invocation against the petitioner along with the provision of Section 122(1-A), qua the petitioner cannot be comprehended, this more particularly for the reason that the show cause notice is issued under section 74 of the CGST Act.

- Section 74 falls under Chapter XV of the CGST Act which pertains to “Demands and Recovery” and provides for “Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilised by reason of fraud or any willful misstatement or suppression of facts”.

- Section 74 is not a penal provision, whereas Section 137 falls under Chapter XIX which provides for ‘offences and penalties’.

- Therefore, as to how such penal provision in Section 137 could be foisted against the petitioner, when the show cause notice is itself a demand cum show cause notice.

- In any event, even assuming that Section 137 could be invoked or is made applicable against the petitioner, then certainly proceedings under section 137 cannot be the proceedings which could be made answerable in a demand cum show cause notice issued under section 74, as such proceedings would be in the nature of a prosecution necessarily involving the applicability of Section 134.

- There cannot be such intermixing of jurisdictions, and that too in foisting a monetary liability as demanded from the petitioner, which on the revenue’s own showing in the show cause notice is alleged to be the liability of the companies.

- For the aforesaid reasons, it is clear from the relevant contents of the show cause notice that the basic jurisdictional requirements / ingredients, are not attracted for issuance of the show cause notice under Section 74 of the CGST Act so as to inter alia invoke Section 122(1-A) and Section 137 against the petitioner.

6. Order

Hon’ble High Court held that the impugned show cause notice is rendered bad and illegal, deserving it to be quashed and set aside.