Form FC-TRS is one of the 9 essential forms required for FDI filing, but what is it, and how to file it? In this article, you will find the answer to all your questions regarding what is an FC-TRS Form, and how to file it.

1. What is Form FC-TRS?

Form FC-TRS stands for ¨Foreign Currency-Transfer of Shares¨. The FC-TRS form is used for reporting of transaction of transfer to Authorised Dealer bank (AD Category-1 Bank).

2. When does Form FC-TRS is required to be filed?

- Since Form FC-TRS is related to reporting of an Foreign Direct Investment translation therefore, the same is required to be filed only when a Non-resident is involved in a transaction.

- Therefore, Form FC-TRS is required to be file for transfer of capital instruments by way of sale in accordance with FEMA guidelines in following cases:

- a Non-resident, holding capital instruments of Indian company on a repatriable basis, transfer it to Non-resident holding such capital instruments on a non-repatriable basis;

- a non-resident, holding capital instruments in an Indian company on non-repatriable basis, transfers it to Indian resident holding capital instruments on repatriable basis;

- a Non-resident, holding capital instruments in an Indian company, on repatriable basis transfers it to Indian Resident.

- an Indian Resident, holding capital instruments in an Indian company, transfers it to Non-Resident holding such capital instruments on a repatriable basis.

* Repatriation Basis: Repatriation basis means when sales or maturity proceeds of investment, net of taxes, are eligible for transfer out of India.

3. In which cases Form FC-TRS is not required to be filed?

For the Following transactions, the FC-TRS form is not required to be filed:

- A non-resident, holding capital instrument of an Indian Company on Non-repatriable basis, transfers it to resident and vice versa.

- A non-resident, holding capital instrument of an Indian Company on repatriable basis, transfers it to resident on repartiable basis.

- Transfer of capital instruments by way of gift.

Therefore, different scenarios of transfer of capital Instrument can be summarised below;

| S. No. | Transferor | Transferee | Whether form FC-TRS is required to be filed or not? (Yes/No) |

| 1 | Non-Resident (Holding capital Instruments on a Non-repatriable basis) | Non-Resident (Non-repatriable basis) | |

| 2 | Non-Resident (Repatriable basis) | ||

| 3 | Non-Resident (Non-repatriable Basis) | Resident (Non-repatriable basis) | Not Required |

| 4 | Resident (Repatriable basis) | Yes | |

| 5 | Non-Resident (repatriable basis) | Non-Resident (Non-repatriable basis) | Yes |

| 6 | Non-Resident (Repatriable basis) | No | |

| 7 | Non-Resident (repatriable Basis) | Resident (Non-repatriable basis) | Yes |

| 8 | Resident (Repatriable basis) | Yes | |

| 9 | Resident (Non-repatriable basis) | Non-Resident (Non-repatriable basis) | Not Required |

| 10 | Non-Resident (Repatriable basis) | Yes | |

| 11 | Resident (Non-repatriable Basis) | Resident (Non-repatriable basis) | No, No Non-resident involved |

| 12 | Resident (Repatriable basis) | No, No Non-resident involved | |

| 13 | Resident (repatriable basis | Non-Resident (Non-repatriable basis) | |

| 14 | Non-Resident (Repatriable basis) | Yes | |

| 15 | Resident (repatriable Basis) | Resident (Non-repatriable basis) | No, No Non-resident involved |

| 16 | Resident (Repatriable basis) | No, No Non-resident involved |

4. For which type of capital instruments does form FC-TRS is required to be filed?

For a transaction in the following capital instrument is required to be reported in Form FC-TRS:

- Equity Shares

- compulsorily and mandatorily convertible preference shares (CMCPS)

- Debentures.

5. Who is liable to file the FC-TRS Form?

Following persons are liable to file Form FC-TRS:

- When any resident is involved in the transaction of transfer of share then such resident whether transferor or transferee and

- When no resident is involved in transaction, Non-resident holding capital instruments on a non-repatriable basis

6. What is the time limit for filing FC-TRS Form?

The Authorised Dealer bank must receive the form FC-TRS within 60 days from earlier of the following dates:

- Date of the transfer of capital instruments or

- Date of receipt/remittance of funds.

7. Procedure to File FC-TRS Form

The FC-TRS form needs to be filed with the Authorized Dealer bank within sixty days of the transfer of capital instruments or receipt/remittance of funds, whichever is earlier. Here you can find the procedure to file FC-TRS Form briefly explained, step by step, for your advantage:

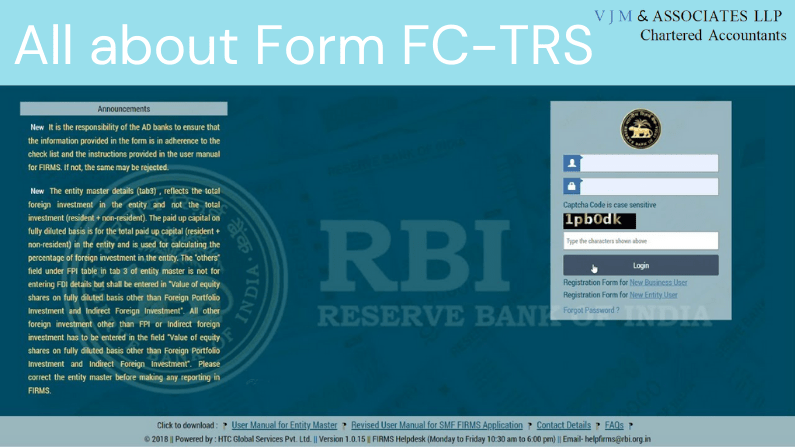

Step 1: Registration for Business User (BU)

- Firstly, person liable to file FC-TRS is required to register himself on FIRMS website at https://firms.rbi.org.in as “Business User”.

- Next, click on registration for new business users and fill up the details in the form as required. [NOTE: Make sure to keep your username unique]. Details of the Investee Company is required to be provided at the time of creating a Business User Account.

- After filling the form the BU has to submit the same.

- Following submission, the document must be confirmed by the AD Bank Branch in question. The approval or rejection of the proposal would be informed to the BU through email.

Step 2: Logging in to firms

- Visit https://firms.rbi.org.in for logging into FIRMS.

- There by using the User Name and default password, given via an email, the BU will can set a new password.

- Logging in to FIRMS will lead the BU to his/her workspace.

Step 3: Log into SMF and reach out to your workspace.

- Post login at FIRMS portal, Under “File Return”, list of all forms shall appear under “Return Type”.

Step 4: Select the Return type

- Select “Form FC-TRS” and click on ¨Add New Return¨.

- Complete form is divided into following 2 parts:

- Common Investment Details

- Form FC-TRS (Which is further Divided into 3-4 tabs)

Step 5: Common investment details

- Details of Common Investment are required to be provided.

- Information provided in this tab is common to all returns that are filed under Single Master Form (“SMF”)

- Information to be provided under this tab:

| Field Name | Description |

| CIN, Company Name, and PAN Number | Pre-filled as per Investee details provided at the time of creating Business User Profile. |

| Application date | Pre-filled, non-editable, system date |

| Entry Route of received FDI* | Select Automatic Route or Government Route, as applicable. In the case of the Government route, government approval is required to be attached to FC-TRS Form. |

| Applicable Sectoral cap/ Statutory ceiling | Applicable sectoral cap as per FEMA 20(R). Clarification: where the company belongs to a sector with mixed entry routes, for eg: Abc pharmaceuticals beyond up to 100% under the Government route and 74% is under the automatic route, the applicable sectoral cap would be 100%. |

| Whether the foreign investment received is for a specific project/ manufacturing unit/ plant? | Select Yes or No as applicable. If yes is selected then additional information of PIN Code, State, City/District, and Brownfield/Greenfield is also required to be provided. |

Step 6: Common details

- After filling in the details of common investment, then Form FC-TRS shall appeal and certain Common details are required to be provided under First Tab.

- Following information is required to be provided

| Field name | Description |

| Transfer by way of | Select sale or Gift, as the case may be |

| Whether the change in the shareholding pattern due to this transaction being reported has already been accounted in the pre-transaction shareholding pattern:* | Select Yes or No. In case ‘Yes’ is selected then there will not be any change in the shareholding pattern for this transaction being reported. In case ‘No’ is selected changes are reflected in the shareholding pattern for this transaction is reported accordingly. |

| Transfer from | Select from the following options as applicable: Resident to Non-resident (including NRI/OCI on repatriable basis)Non-resident (including NRI/OCI on repatriable basis) to ResidentNRI /OCI/eligible investor on a non-repatriable basis to Non-resident (including NRI/OCI on repatriable basis)Non-resident (including NRI/OCI on repatriable basis) to NRI/OCI/eligible investor on non-repatriable basis. |

| Transfer Type | Select from the following options as applicable: Transfer as per Regulation 10(3) of FEMA 20(R)-Sale of capital instruments from a person resident outside India to a person resident in IndiaTransfer as per Regulation 10(4) of FEMA 20(R)-Sale of capital instruments from a person resident in India, including NRI/OCI or eligible investor under Schedule 4 to FEMA 20(R) to a person resident outside India transfer as per Regulation 10(5) of FEMA 20(R)-Gift of capital instruments from a person resident in India, including NRI/OCI or eligible investor under Schedule 4 to FEMA 20(R) to a person resident outside India transfer as per Regulation 10(12) of FEMA 20(R)-Invocation of pledgeTransfer of capital instruments as per Regulation 3 to FEMA 20(R)Others (please specify) |

| Date of Transfer | Select the date of transfer from the calendar. (In case the date of transfer is after the date of filing of FC-TRS form i.e future date, select the date as application date and provide the date of transfer as per the Transfer agreement as an attachment under “Other Attachments”). |

| Nature of Transfer | Select from the following options as applicable: Offer for sale in an IPO/ FPOPrivate arrangements was of capital instrumentsSale on the stock exchange other than those under Schedule 2 and Schedule 3 of FEMA 20(R)Purchase on the stock exchange other than those under schedule 2 and Schedule 3 of FEMA20(R)Participating interests/rights in oil fieldsMerger / Demerger / AmalgamationBuy black invocation of pledge other (please specify) NOT applicable for Transfer by Gift |

| Buyer and Seller details for sale or Donee and Donor details for gift | Fill up the buyer and seller details for transfer by sale or Donee and Donor details for Transfer by Gift. |

Step 7: Particulars of transfer

- Under Next tab, following information related to transfer is to be provided:

| Field Name | Description |

| Type of capital instrument | Type of capital instrument shall be selected from the drop-down menu. In case of a gift, if the shares are transferred select as “Shares transferred as Gift”, if not, then the capital instrument as transferred |

| Number of Instruments | Enter the number of instruments as transferred. |

| Conversion ratio | In the case of Equity shares, partly paid-up shares, shares transferred as Gifts, participating interest/rights in oil fields enter as 1:1. For CCDs /CCPs/ share warrants enter the pre-fixed upfront conversion ratio. In case there is no upfront conversion ratio enter the ratio as per the maximum permissible conversion of CCDs/CCPs/share warrants into equity shares in compliance with the pricing guidelines. |

| Number of equity shares on a fully diluted basis | Auto-populated as per the conversion ratio and the number of instruments |

| Face value | Enter the face value of the equivalent equity shares. In case of CCDs/CCPs /share warrants- DO NOT enter the face value of the instrument as it will not give the correct shareholding pattern. For participating, interests/rights in oil fields enter the value as 0 (zero). |

| Transfer price per instrument | Enter Transfer price. For Gift, enter transfer price as 0 (zero). |

| Total amount consideration | Auto-calculated as the Number of instruments multiplied by transfer price per instrument. |

| “ADD” button | Click on the ADD button and check that all details are reflected in the adjoining table. In case of multiple instruments being transferred, repeat the above process. Information can be modified by clicking on the “Edit” Icon and can be deleted through “Delete Icon”. |

| Fair value of the capital instruments at the time of transfer | Enter the fair value. valuation certificate from the authorized person and Transfer agreement (relevant extracts) along with the consent letter of buyer and seller at “Valuation certificate.” shall also be attached. In the case where multiple instruments are being transferred, enter the fair value of one instrument and attach a clarificatory letter along with the valuation certificates at the attachment “Valuation certificate”. |

Step 8: Remittance details

- Details about remittance of consideration is to be provided under this tab. This tab shall not apply in cash of transfer through gift.

| Field Name | Description |

| Mode of payment | Select from the drop-down menu |

| Name and address of AD bank | The name of the bank and address can be selected from a given list. |

| Amount remitted/received in Rs | Amount in Rs as being received or remitted in this reporting |

| Whether and Tranche number | Step-1: Select from the drop-down menu payment on full consideration here, date of remittance in a future date. It may be left blank. Enter the tranche number as 1 (one). Payment on a deferred basis in case it is first tranche payment, enter tranche number as 1 (one)In case it is 2,3,4…..etc tranche: enter accordingly. Further, enter FC-TRS reference number along with tranche amount reported in FC-TRS, under “FC-TRS Details” Indemnity arrangements case it is first FC-TRS reporting: Here, the date of remittance is the date on which the amount is received. If it is a future date- it may be left blank. In case it is first FC-TRS reporting for reporting indemnity payment: Enter Tranche number as 2 (two). Under FC-TRS details you must enter the FC-TRS reference number, along with the tranche amount reported in FC-TRS. |

| Whether the remitter is different from a foreign investor | Select “NO”, if the remitter is the same. In other cases, Select “YES” and enter the details viz., Name of the Remitter, Country of remitter, the relationship between Remitter and foreign investor and attach the requisite documents |

| Declaration | A declaration is to be provided that complete and accurate information has been provided. |

Step 9: Shareholding pattern.

This is the second last step where you will have to submit the following details related to a shareholding pattern:

- Other than Foreign Portfolio Investment and indirect foreign investment, the value of equity shares on a fully diluted basis is the value of capital contribution/profit shares, Foreign Portfolio Investment, and indirect foreign investment.

- Pre-transaction values are auto-populated from the Entity Master (tab 3)

- Post-transaction values are determined automatically depending on the information entered in the form. [Pre transaction value of shares + value of shares reported in the form=post transaction value of shares.]

- The Business user must ensure that the form’s details are valid in order for the auto-calculated shareholding pattern to be accurate.

Step 10: Submitting the form

- When you’ve finished filling out all of the fields, click Save and Submit to submit the form.

- If you are a non-resident transferor/transferee, you must submit a declaration in the given format.

8. List of Documents to be attached along with the Form FC-TRS

Along with your FC-TRS Form, you will have to attach the following documents:

8.1 For transfer by way of Gift

- Relevant Regulatory Approvals: Wherever required, these documents need to be attached as ¨other documents¨ with the FC-TRS Form.

- Consent Letter: This is the consent letter signed between the donor and the donee for the transfer.

- Non-Resident Declaration: As per the given format mentioned above, it needs to be attached with the FC-TRS Form.

8.2 For transfer by way of Sale

- Transfer Agreement: Relevant excerpts of the transfer agreement, as well as the consent letter between buyer and seller for the sale/purchase on stock market, must be attached to the FC-TRS Form. These contract notes might be included in the “Transfer agreement/Valuation certificate” section.

- Valuation Certificate: A valuation certificate as per FEMA 20 (R) needs to be attached at “Transfer agreement/Valuation certificate” along with the FC-TRS Form.

- Non-Resident Declaration: As per the format mentioned above, non-resident declaration needs to be attached.

- In case of sale by a non-resident, acknowledgement of FC-TRS, as applicable for the capital instruments being sold, has to be attached as “other attachment”.

- An FIRC/Outward remittance certificate and KYC needs to be attached at the specified attachment.