Expanding your business into India is a growth opportunity, but it comes with its challenges. As of March 2025, India recorded 19,000 foreign companies, up from 15,000 just a few months earlier, reflecting a surge in international investment.

The process of setting up a business in India can feel daunting for foreign companies, especially when familiar frameworks like U.S. accounting standards don’t apply. From choosing the right business structure to tackling local tax laws and compliance regulations, the complexities can be overwhelming.

This guide walks you through the essentials of registering a company in India, offering practical insights tailored for U.S. businesses. We’ll cover everything from legal requirements to procedures to ensure you understand each step with clarity and confidence.

Company registration in India is the formal process of establishing your business as a separate legal entity under Indian law. Registering a company in India offers key advantages for U.S. businesses looking to expand:

These benefits help establish credibility and create growth opportunities as you expand your U.S. business into India.

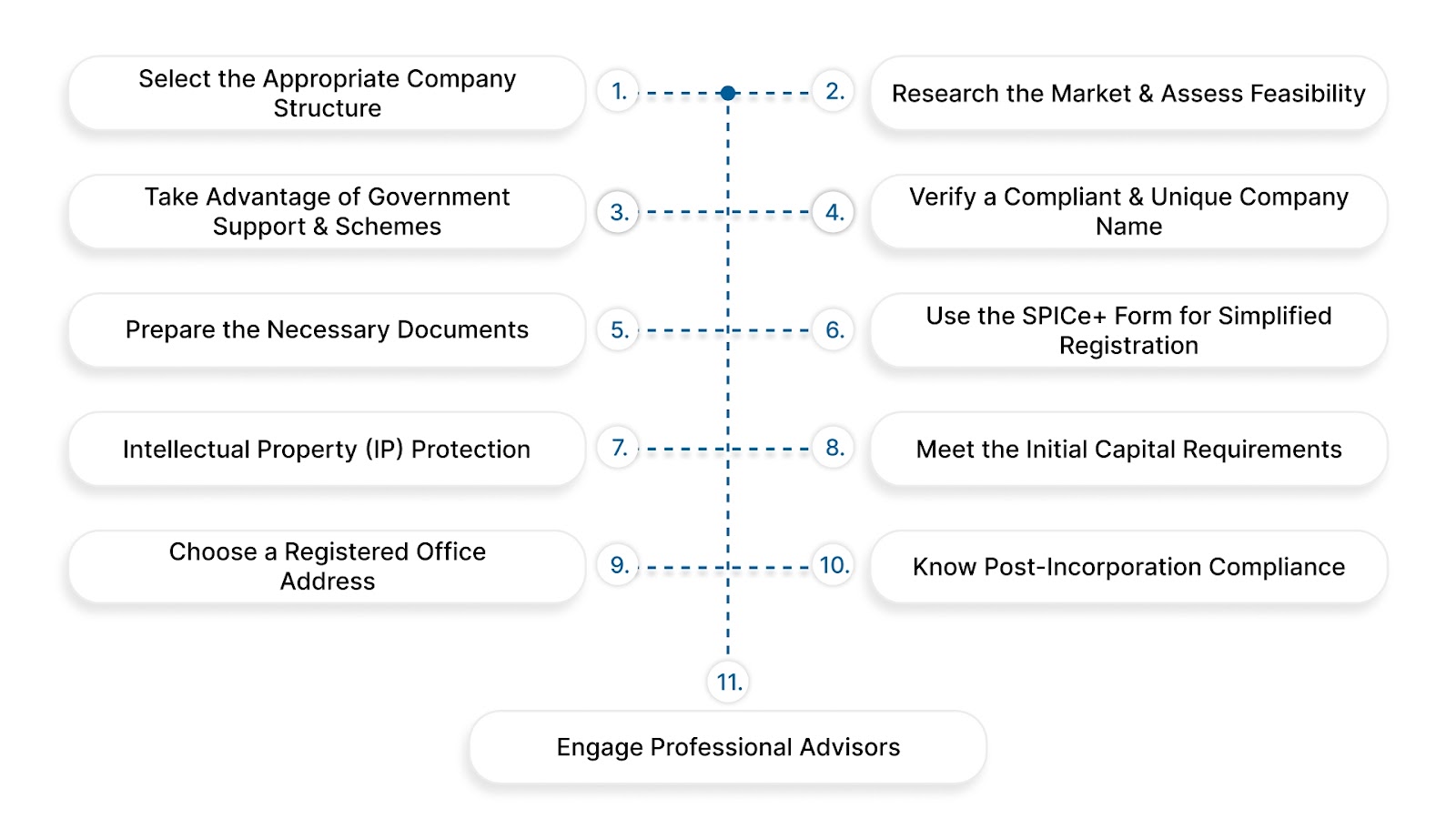

Now that you understand the benefits of registering a company in India, let's look at the steps involved in the registration process.

Starting a business in India as a U.S. company involves a series of strategic decisions and legal steps. Here’s a breakdown of the essential steps:

Your choice of business structure will determine your tax responsibilities, funding options, and liability protection. Common structures include:

For most U.S. companies, a Private Limited Company (PLC) is the best option. It provides limited liability, allows for investment, and offers better operational flexibility.

Also Read: Why Should You Register A Private Limited Company?

Before registering a company, assess market demand for your products or services. Use tools like Google Trends or social media analytics to gauge consumer interest and the competitive environment. If you're entering a regulated sector like finance or healthcare, research local compliance standards to avoid potential hurdles.

For example, if your U.S. business deals with healthcare products, you must comply with India’s Drugs and Cosmetics Act, which differs from FDA regulations in areas like product approvals and labeling. Understanding these differences is key to ensuring compliance and avoiding delays.

The Indian government offers various programs to support new businesses, such as Startup India, which provides funding, tax exemptions, and regulatory relief. These programs can offer U.S. companies valuable incentives, helping them lower initial costs and reduce compliance burdens.

Selecting a unique company name is essential to avoid future legal issues. Your business name should reflect your business operations and comply with India's naming regulations. The name must not conflict with existing trademarks or company names in India. Use the Ministry of Corporate Affairs (MCA) website to check availability.

For a smooth registration process, gather all essential documents:

These documents ensure that your company meets legal standards and complies with Indian regulations.

The SPICe+ form simplifies company registration by combining several steps into one application, including name approval, DIN allotment, and incorporation. Filling out this form correctly will save you time and reduce errors during registration.

Protect your intellectual property in India by registering patents, trademarks, and copyrights. The Indian IP system offers strong protection, preventing unauthorized use of your brand and innovations.

Although there’s no minimum capital requirement for a Private Limited Company, it’s crucial to declare adequate authorized capital. This capital covers initial operational costs until the business becomes self-sustaining.

For U.S. companies, the capital should be enough to cover initial business setup costs, such as office rent, legal fees, and staff recruitment.

Also Read: Company Registration Cost in India Explained

A registered office address is required for official communications. This address can be residential, industrial, or commercial, but it must be a real location within India. Government correspondence will be sent to this address, so it’s essential that it is accurate and accessible.

Once your company is registered in India, several critical legal steps must be completed to ensure full compliance with Indian regulations.

These include opening a business bank account, registering for Goods and Services Tax (GST) (if applicable), and obtaining a Permanent Account Number (PAN) and Tax Deduction and Collection Account Number (TAN). These steps are similar to securing your EIN and state-level registrations when establishing a business in the U.S.

Additionally, you'll need to maintain compliance with the Registrar of Companies (RoC) by submitting regular reports and fulfilling other regulatory obligations.

Tackling Indian business regulations can be challenging, especially for foreign investors. At VJM Global, we provide expert guidance tailored to U.S. businesses looking to expand into India.

Our team can assist with compliance, financial management, and understanding India's regulatory environment, ensuring a smooth, efficient market entry. Get started today.

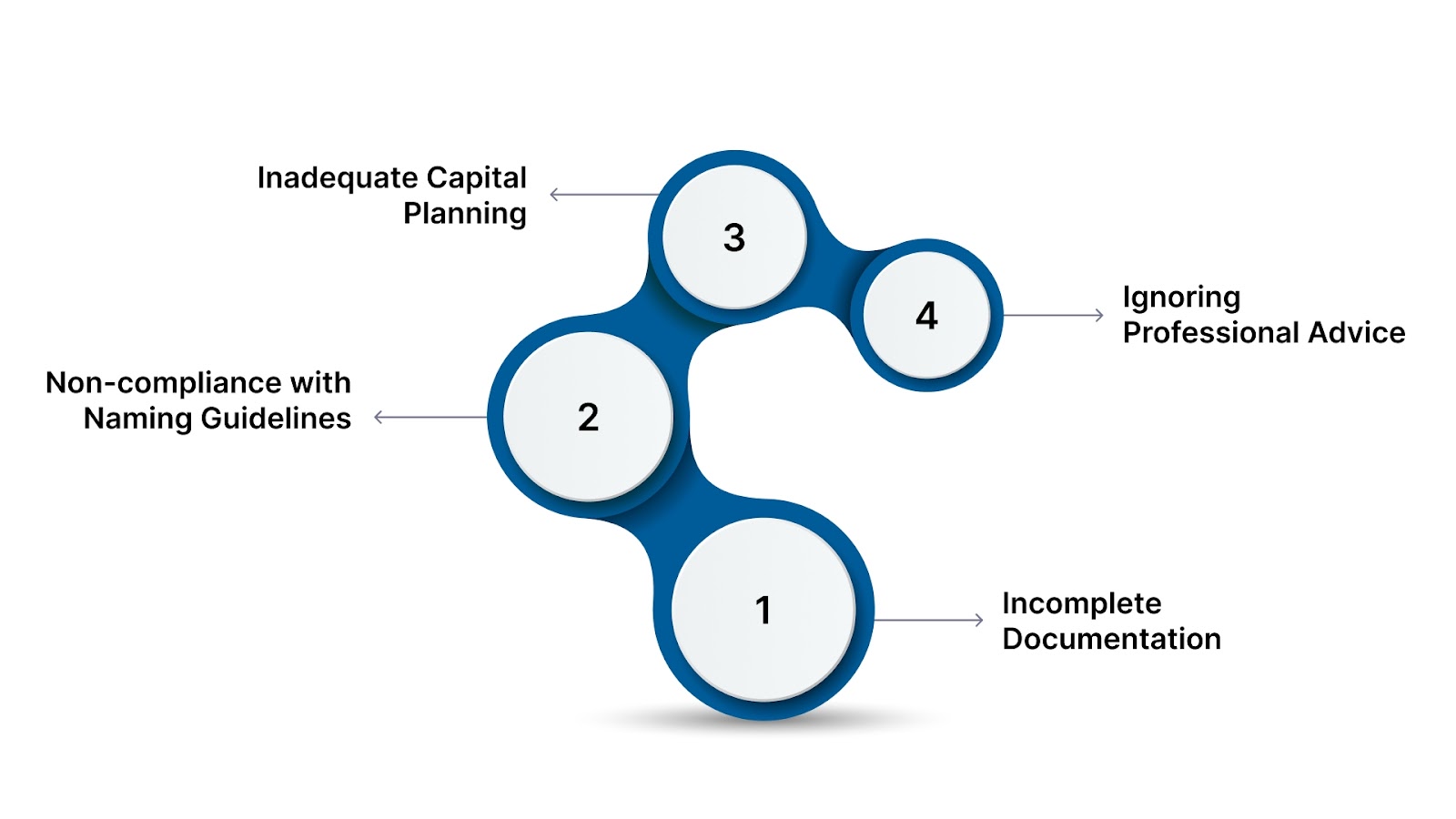

With the steps in mind, it's important to be aware of the common pitfalls that could delay or complicate your registration.

Starting a business in India offers immense opportunities, but it’s crucial to handle the registration process carefully to avoid pitfalls that can cause delays.

Let VJM Global guide you through the complexities of setting up your business in India. Our expert team will ensure your operations run smoothly and comply with all local regulations. Contact us today for tailored advice and reliable support every step of the way.

By being aware of these common pitfalls, U.S. businesses can avoid costly mistakes and set up their operations in India more smoothly.

Now that you know the process and how to avoid common mistakes, here’s how VJM Global can help you get started on your journey to registering your company in India.

At VJM Global, we provide expert support for U.S. businesses looking to register and establish operations in India. Here’s how we can help:

Let VJM Global guide you through every step to ensure a successful market entry.

Expanding into India opens up exciting opportunities, but it requires more than just good execution. Understanding the complexities of local regulations, compliance, and tax laws is essential to avoid setbacks. For U.S. businesses, getting the right support can make all the difference in ensuring a smooth and successful market entry.

At VJM Global, we’re here to guide you through every stage of your journey, from company registration to ongoing compliance, ensuring that your business thrives in the Indian market

Let’s make your business expansion a success. Contact VJM Global today for tailored guidance, expert advice, and seamless support in registering and setting up your company in India.

In India, anyone can register a company, but the type of company registration depends on the business structure. Each business must comply with legal and tax requirements to be eligible for registration.

Yes, Non-Resident Indians (NRIs) can register businesses in India. However, they must follow specific guidelines under the Foreign Direct Investment (FDI) policy. NRIs cannot register sole proprietorships or partnership firms, but they can establish Private Limited or Public Limited companies.

To register a company in India, you will need several key documents, including:

There is no minimum capital requirement for most types of companies in India, especially for a Private Limited Company. However, it is recommended to have sufficient capital to support initial operations and maintain smooth cash flow.

The type of business structure depends on your company’s goals and scale. Most foreign investors opt for a Private Limited Company because it offers limited liability protection, greater credibility, and is easier to manage with fewer restrictions. A Public Limited Company is suitable for large-scale operations.