India’s growing global presence means more residents are investing abroad, sending children overseas for education, and supporting families across borders. To simplify these international transactions, the Reserve Bank of India introduced the Liberalized Remittance Scheme (LRS), a framework that allows individuals to legally and safely remit money outside India.

According to the RBI, outward remittances under LRS reached USD 30 billion in FY 2023–24, with education, travel, and investments being the top contributors. With demand rising every year, understanding the LRS is no longer optional; it’s essential.

This guide explains everything you need to know about the Liberalied Remittance Scheme, including eligibility, permissible uses, prohibited transactions, taxation, and the step-by-step remittance process.

At a Glance

Money can be used for education, travel, medical needs, investments, gifts, or family support.

Prohibited transactions include lottery purchases, forex margin trading, and dealings with FATF blacklisted countries.

From Budget 2025, no TCS up to ₹10 lakh; above this, 5% TCS applies (except education loans).

Remittances require PAN, Form A2, and KYC compliance, and must be routed through an RBI-authorised dealer bank.

LRS provides flexibility to diversify investments abroad while ensuring compliance with FEMA and RBI guidelines.

What is the Liberalized Remittance Scheme (LRS)?

The Liberalized Remittance Scheme (LRS) is a facility introduced by the Reserve Bank of India (RBI) under the Foreign Exchange Management Act (FEMA), 1999. It allows resident individuals to remit money abroad for specific permitted purposes without prior RBI approval. With a yearly limit of USD 250,000 per individual, LRS provides Indian residents with the flexibility to meet personal, educational, medical, and investment needs globally.

Key Features of LRS

Remittance Limit: Up to USD 250,000 per financial year for each resident individual.

Eligible Individuals: Available to resident individuals, including minors (through guardians).

Permissible Uses: Education, travel, medical treatment, investment in foreign assets, gifts, donations, and maintenance of close relatives abroad.

Prohibited Transactions: Cannot be used for lottery tickets, forex margin trading, or dealings with FATF non-compliant countries.

No RBI Approval Needed: Remittances under LRS for permitted purposes do not require prior RBI approval.

Regulated by FEMA: Ensures compliance with India’s foreign exchange laws.

Tax Implications: Subject to Tax Collected at Source (TCS) based on transaction type and amount.

Now that we’ve understood what the Liberalized Remittance Scheme (LRS) is and its key features, let’s look at some of the most common ways Indian residents can use it.

Permissible Uses of Liberalized Remittance Scheme

The Liberalized Remittance Scheme gives Indian residents the freedom to use remittances for a wide range of legitimate personal and financial purposes. By allowing individuals to invest, study, or support family abroad, LRS opens access to global opportunities while maintaining regulatory safeguards. Here are some common used of lrs:

Education Abroad: Payment of tuition fees, living expenses, and other related costs for studying overseas.

Travel Expenses: Covering personal, business, or leisure travel costs, including boarding and lodging.

Medical Treatment: Payments for hospitalization, medical bills, or healthcare-related expenses abroad.

Investments: Buying shares, debt instruments, real estate, or other permissible foreign assets.

Gifts & Donations: Transferring funds to relatives or charitable organizations abroad.

Maintenance of Relatives: Supporting close family members living overseas.

Transfers to Own Account: Moving funds to personal accounts maintained in foreign banks.

While LRS offers broad flexibility in how funds can be used, it’s equally important to understand who can actually access the scheme and how to apply for it.

Eligibility and Application for Liberalized Remittance Scheme

The Liberalized Remittance Scheme is designed for individuals, not institutions. To ensure compliance, RBI has clearly defined who can apply and what is required before making a remittance. Meeting these eligibility conditions is the first step toward accessing the benefits of LRS.

Who is Eligible?

Resident Individuals: Any resident individual in India, including minors.

Guardians for Minors: A guardian can make remittances on behalf of a minor.

Not Eligible: Corporations, partnership firms, HUFs, trusts, and other entities are excluded.

Application Requirements

Bank Account: Applicant must hold an Indian bank account with an authorized dealer (AD) bank.

Permanent Account Number (PAN): A valid PAN card is mandatory for identification and tax compliance.

Declaration Form: Individuals must submit a declaration confirming the purpose of remittance and compliance with LRS rules.

Supporting Documents: Depending on the purpose (education, medical, travel, etc.), relevant documents such as admission letters, invoices, or medical certificates may be required.

Once you know the eligibility, the next step is understanding how the actual remittance process works. Following the correct procedure ensures smooth transfers and compliance with RBI regulations.

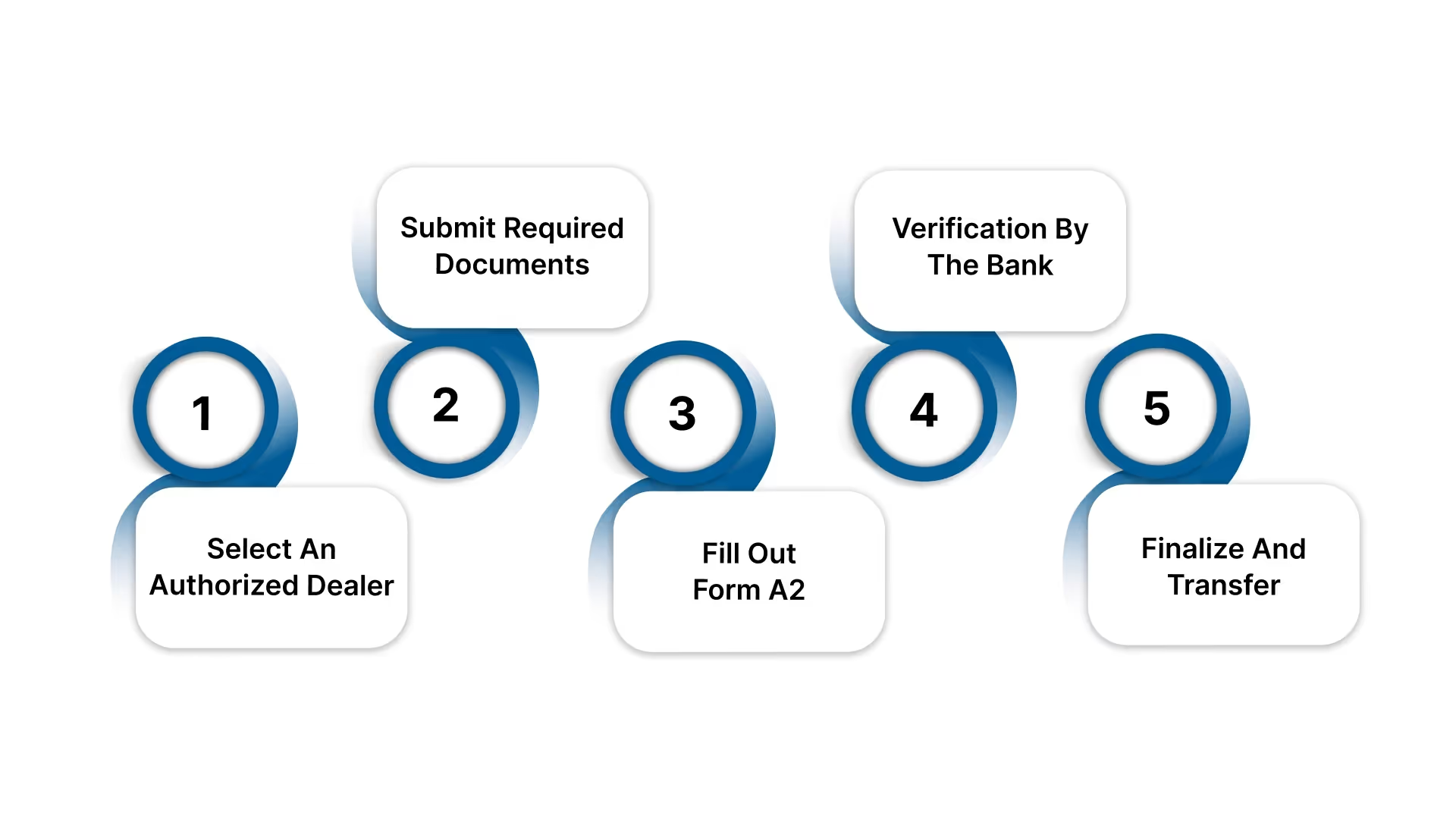

Process of Remittance Under Liberalized Remittance Scheme

Remitting money abroad under the Liberalized Remittance Scheme involves a few structured steps, all of which are handled through authorized dealers (banks).

Select an Authorized Dealer: Choose an RBI-approved bank or financial institution authorized to process foreign remittances.

Submit Required Documents: Provide KYC documents such as PAN card, passport, and bank details, along with declarations as required.

Fill Out Form A2: Complete and sign Form A2, which specifies the purpose and amount of remittance.

Verification by the Bank: The bank will verify details to ensure the remittance falls under permitted categories and is within the USD 250,000 limit.

Finalize and Transfer: Once verified, the funds are converted to the desired foreign currency and remitted abroad.

This streamlined process makes it easier for individuals to send funds abroad while ensuring compliance with FEMA and RBI guidelines.

While the LRS provides flexibility for legitimate remittances, it also has strict boundaries to prevent misuse. Knowing what’s prohibited is just as important as knowing what’s allowed.

Prohibited Transactions Under Liberalized Remittance Scheme

Under the Liberalized Remittance Scheme, residents are not permitted to use funds for the following:

Lottery or Gambling: Buying lottery tickets, sweepstakes, or participating in gambling/betting activities abroad.

Margin Trading & Speculation: Engaging in foreign exchange trading, margin trading, or leveraged investments.

Prohibited Countries: Sending money to entities or individuals located in countries identified by the Financial Action Task Force (FATF) as non-cooperative jurisdictions.

Banned or Illegal Activities: Any transactions that violate Indian law, FEMA, or international regulations.

By clearly outlining these restrictions, the RBI ensures that LRS is used only for genuine personal, educational, medical, and investment purposes.

Outsource your bookkeeping and save time without compromising accuracy. Let us handle the books. Talk to an expert today.

Understanding what you cannot do under LRS is only half the picture. The next crucial aspect is knowing the tax implications and conversion fees that apply to every remittance.

Tax Implications and Conversion Fees

Every outward remittance under LRS carries certain tax and fee considerations that individuals must plan for. Recent updates in the Union Budget 2025 have further refined these rules:

Revised TCS Threshold (Budget 2025): The threshold for Tax Collected at Source (TCS) on foreign remittances under LRS has been raised from ₹7 lakh to ₹10 lakh per financial year. No TCS will apply for LRS transactions up to ₹10 lakh annually.

Educational Remittances: If the remittance is for education and funded through a loan from a recognised financial institution, no TCS will apply, even if the amount exceeds the ₹10 lakh threshold.

Standard TCS Rate: For all other remittances beyond the ₹10 lakh annual limit, a 5% TCS will be levied.

Conversion and Transaction Charges: Alongside taxes, banks apply conversion charges and service fees, which vary by institution and are counted within the USD 250,000 LRS limit.

Refund and Adjustments: Any TCS deducted can be adjusted against your income tax liability or claimed as a refund when filing your ITR. These deductions can be tracked through Form 26AS.

By staying updated with these changes, individuals can better plan their overseas remittances and avoid unnecessary costs.

RBI Guidelines for Outward Remittance under LRS

When transferring funds abroad under the Liberalized Remittance Scheme (LRS), individuals must comply with the guidelines set by the Reserve Bank of India (RBI). These rules ensure that remittances are transparent, legal, and compliant with foreign exchange laws.

Here’s what you need to know:

Mode of Payment: Outward remittances can be made through a demand draft in the name of the individual or the overseas beneficiary.

Foreign Account Option: Individuals can also open and maintain a foreign bank account to manage remitted funds.

Authorised Dealers: Remittances must be routed through a bank branch designated as an authorised dealer by RBI.

Mandatory PAN Requirement: A valid PAN card is required for all outward remittances.

AML & KYC Compliance: Individuals must adhere to Anti-Money Laundering (AML) and Know Your Customer (KYC) guidelines.

Form A2 Submission: Before purchasing foreign currency, individuals must fill out Form A2, declaring the purpose of the remittance.

Credit Facilities Prohibited: Banks are not allowed to extend any credit facilities to residents under the LRS.

Following these RBI-prescribed steps ensures that your outward remittances are smooth, compliant, and risk-free.

After exploring the rules, processes, and restrictions of LRS, it’s equally important to highlight the advantages and flexibility this scheme brings to Indian residents.

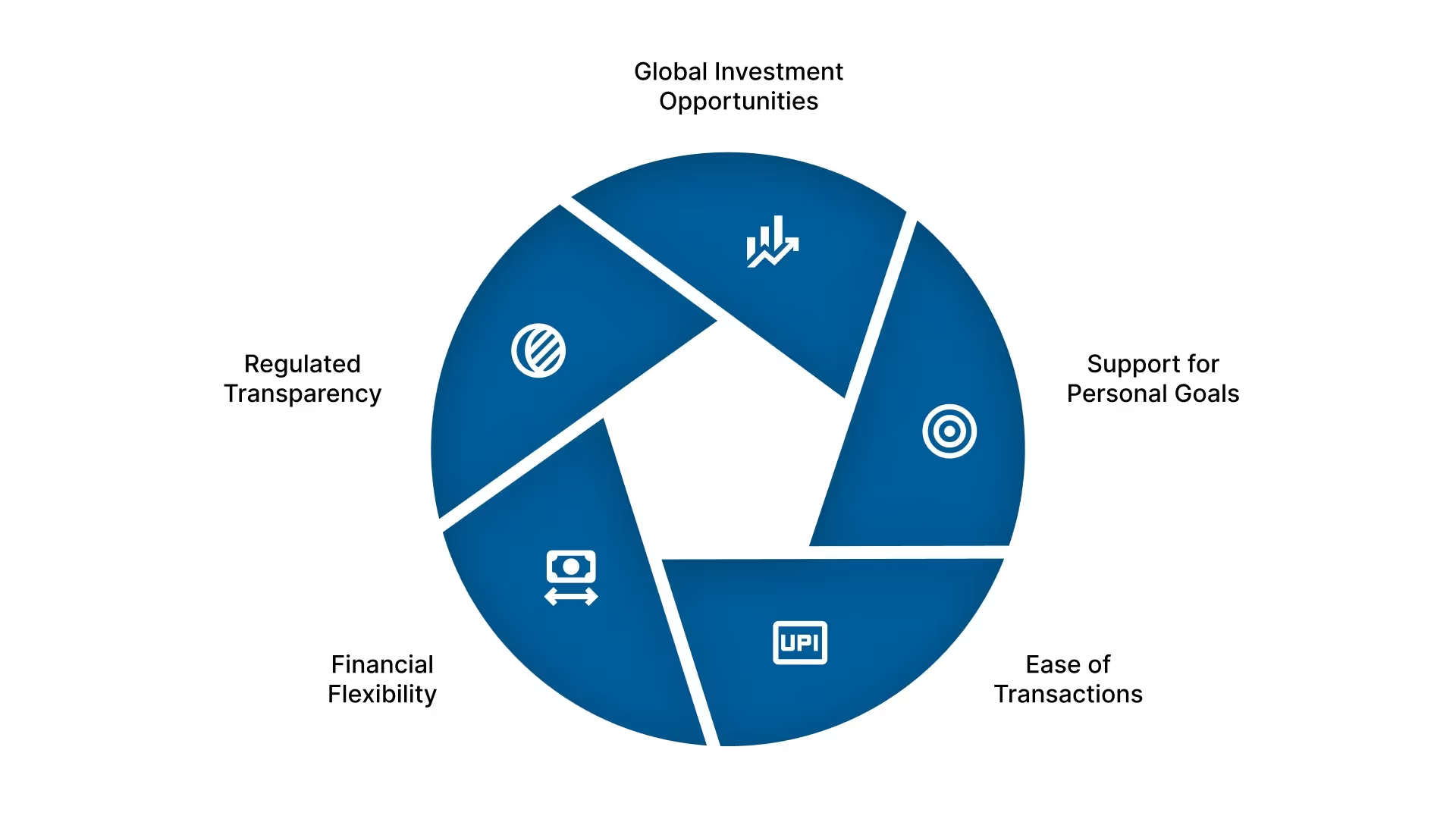

Benefits and Flexibility of the Liberalized Remittance Scheme (LRS)

One of the biggest advantages of the LRS framework is the freedom it offers Indian residents to use their money abroad without needing prior RBI approval for most transactions. It not only supports personal needs but also provides scope for global investments and diversification.

Key Benefits:

Global Investment Opportunities: Individuals can diversify their portfolios by investing in international stocks, bonds, real estate, or other permitted assets.

Support for Personal Goals: Whether it’s funding overseas education, medical treatment, or family maintenance, LRS makes cross-border financial planning much easier.

Ease of Transactions: No prior RBI approval is required for permitted transactions, reducing red tape and saving time.

Financial Flexibility: Residents can open and maintain foreign currency accounts, giving them more freedom in managing money internationally.

Regulated Transparency: Since all transactions go through authorised dealers, compliance with FEMA, 1999 ensures both safety and accountability.

In essence, the Liberalized Remittance Scheme acts as a bridge for Indians to participate confidently in the global economy while staying within regulatory boundaries.

Challenges People Face with Liberalized Remittance Scheme LRS (and Solutions)

While the Liberalized Remittance Scheme provides flexibility for global transactions, individuals often encounter practical hurdles when using it. Understanding these challenges and their solutions can make the process smoother:

Complex Documentation Requirements

Challenge: Many residents find the documentation process, PAN, Form A2, and bank verification overwhelming.

Solution: Working with an experienced bank officer or financial advisor ensures all forms are completed accurately and delays are avoided.

High Conversion Fees and Charges

Challenge: Currency conversion rates and bank charges can significantly reduce the value of remittances.

Solution: Compare rates among authorized dealers before initiating transfers and use banks offering competitive foreign exchange services.

Confusion Over TCS Rules

Challenge: Frequent changes in Tax Collected at Source (TCS) thresholds leave many individuals uncertain about their tax liabilities.

Solution: Stay updated on the latest Budget announcements and consult tax advisors to claim refunds or set off TCS against ITR correctly.

Restrictions on Certain Transactions

Challenge: Many residents are unaware of the prohibited activities under LRS, such as margin trading or lottery purchases, leading to compliance risks.

Solution: Always confirm with your bank whether your intended remittance is permissible under RBI’s guidelines before initiating the transfer.

Delays in Processing

Challenge: Remittance requests may sometimes take longer due to compliance checks or incomplete paperwork.

Solution: Submitting accurate information upfront and maintaining clear communication with your bank reduces the risk of delays.

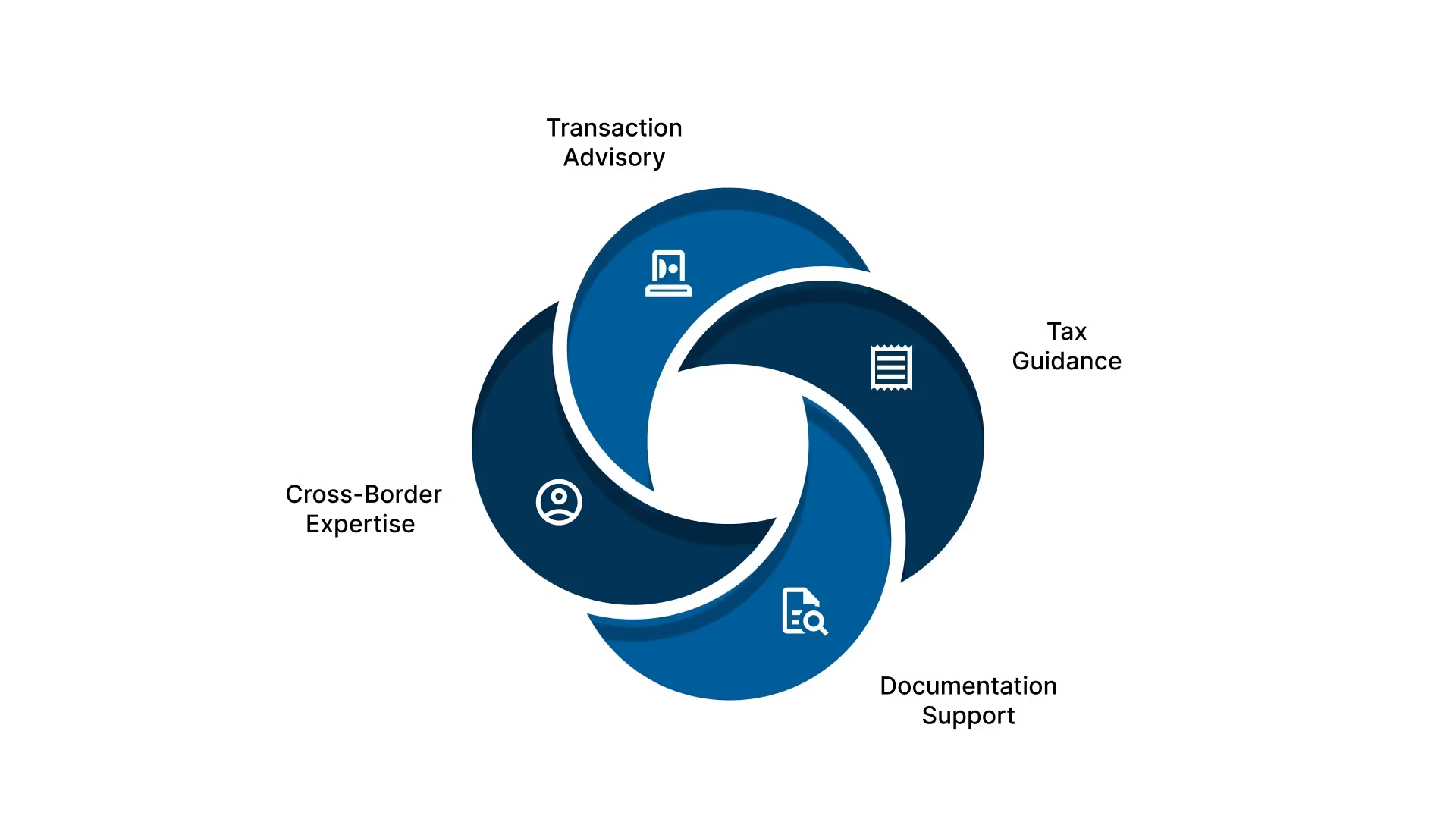

How VJM Global Helps You with LRS Compliance

Managing the Liberalized Remittance Scheme (LRS) can be complex, with evolving RBI guidelines, tax rules, and documentation requirements. Missteps can delay your transfers, trigger unnecessary tax costs, or even create compliance issues.

VJM Global simplifies this process for individuals and businesses by offering end-to-end support:

Transaction Advisory: Clarifying permissible vs. prohibited uses to ensure every remittance aligns with RBI guidelines.

Tax Guidance: Helping you manage TCS, claim refunds, and plan remittances for maximum tax efficiency.

Documentation Support: Preparing and submitting Form A2, KYC, and related paperwork seamlessly with your bank.

Cross-Border Expertise: Streamlining remittances for education, healthcare, investments, or family support across jurisdictions.

With our guidance, you can focus on your goals while we take care of the compliance and regulatory details.

Free up your team's time, outsource accounting to VJM Global and focus on growth.

FAQs

1. Who is eligible to use the Liberalized Remittance Scheme (LRS)?

LRS is available to resident individuals in India, including minors. However, it is not applicable to corporates, partnership firms, trusts, or HUFs.

2. What is the maximum limit allowed under LRS?

As per current RBI rules, resident individuals can remit up to USD 250,000 per financial year for permissible transactions such as education, healthcare, travel, or investments.

3. Do I need RBI approval for outward remittances under LRS?

No prior RBI approval is required for remittances within the prescribed limit for permitted purposes. However, the transaction must comply with FEMA regulations and bank documentation requirements.

4. How is Tax Collected at Source (TCS) applied to LRS transactions?

As per Budget 2025, no TCS applies on LRS transactions up to ₹10 lakh annually. Beyond this limit, a 5% TCS is applicable, except when funds are remitted for education through approved loans.

5. Can I remit money abroad for investments under LRS?

Yes, LRS allows investment in foreign assets such as stocks, debt instruments, mutual funds, and even property, provided the total does not exceed the USD 250,000 annual limit.

CA Kapil Mittal

Mr. Kapil Mittal is a partner of the firm and has a strong legal and tax background with over 15 years of experience. He heads the Firm’s Tax Advisory and Compliance Practice. He specializes in