.jpg)

Starting a business in India offers compelling opportunities for U.S. investors, but the path to success can seem complex without clear direction. It takes 12-18 days to register a business, but the process involves multiple steps. From selecting the right structure to meeting legal and compliance requirements, each stage requires careful attention.

Fortunately, many sectors allow up to 100% Foreign Direct Investment (FDI) through an automatic route, eliminating the need for prior government approval. While the regulations are welcoming, the complexity of local laws, taxes, and compliance requirements can make the process tricky.

This blog will guide you through the essential steps to set up a business in India. We’ll provide actionable insights to simplify the process, covering the legal framework and cost considerations, and setting up a one-person company. Let’s get started.

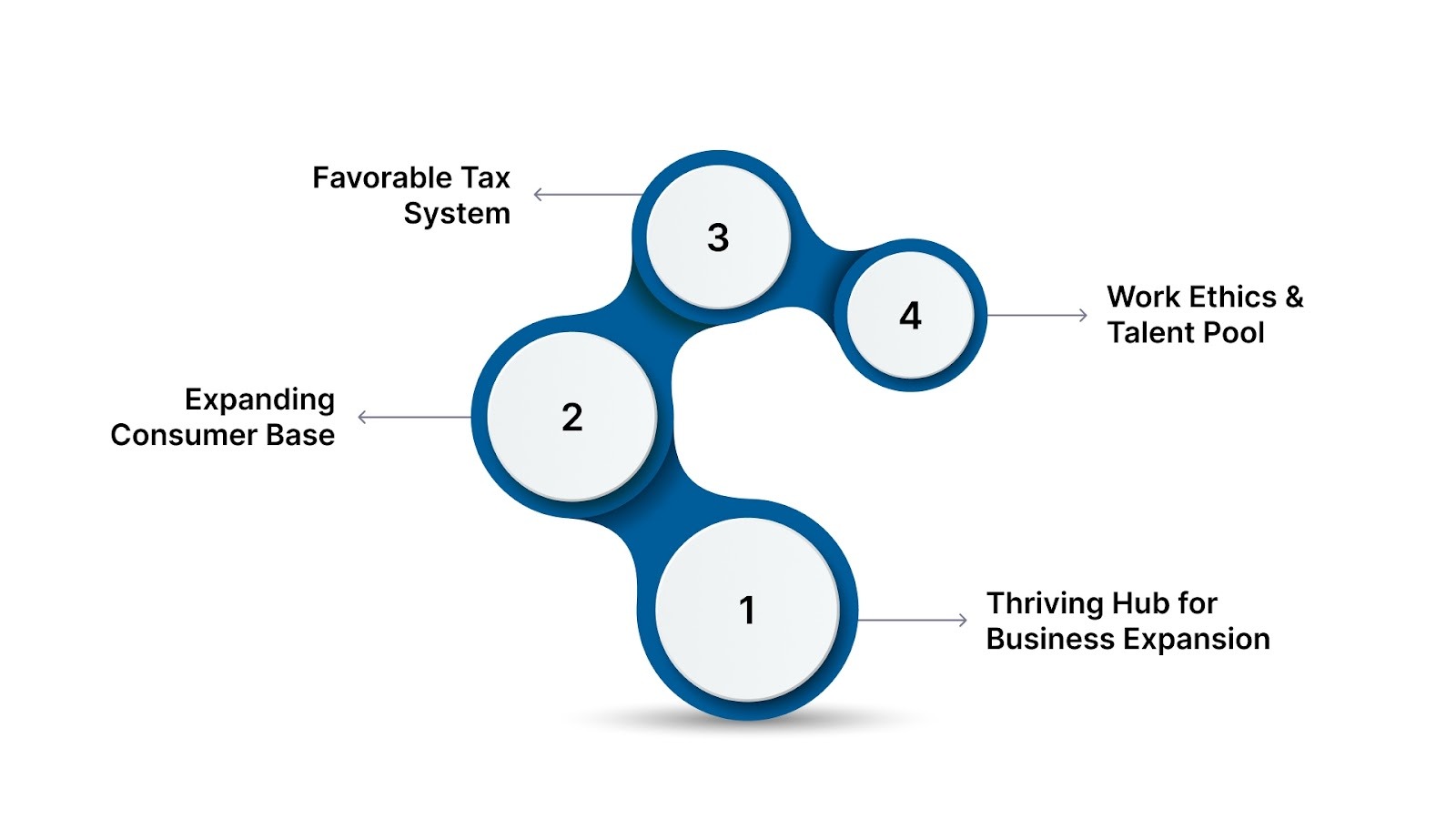

Alt text: Advantages for Foreign Companies to Set Up in India

India offers an array of compelling advantages for foreign companies looking to establish themselves in one of the world’s most dynamic and rapidly growing markets.

India offers immense opportunities for global companies, driven by its steady economic growth and growing consumer market. With a forecasted 6.8% GDP growth in 2025, India remains one of the fastest-growing major economies globally, offering a favorable environment for business expansion.

FDI inflows exceeded $50 billion in FY 2024-25, a 13% increase from the previous year. In Q1 FY 2025-26, FDI rose 15%, signaling investor confidence, especially in the tech sector. With strong GDP growth and rising FDI, India is a dynamic and promising market for global business expansion and investment opportunities.

India, with a population exceeding 1.4 billion, is the fourth-largest economy in Asia and presents vast opportunities for foreign companies. Its large and youthful population, with a median age of just 28, ensures an energetic workforce and growing consumer base.

For U.S. manufacturers, this demographic advantage translates into a ready labor pool and a growing market for products. In addition, India’s expanding education and skill development programs ensure a steady supply of specialized talent for manufacturing needs.

India boasts a network of tax treaties designed to support international business. Recent updates to tax codes and the introduction of GST have simplified operations for foreign investors. This reform makes tax compliance smoother and more predictable, encouraging further investment in the country.

This change is similar to the U.S. Tax Reform Act of 1986, which streamlined the tax system by reducing brackets and eliminating certain deductions. Just as the reform aimed to simplify tax compliance, India’s GST creates a more business-friendly environment by reducing administrative burdens for foreign investors.

The Indian workforce is known for its hardworking, innovative spirit, with a large proportion of the population in the working-age group (15-64 years). This factor, combined with a pool of talent in fields such as IT, engineering, and pharmaceuticals, gives foreign businesses a competitive edge in scaling operations efficiently.

By taking advantage of these key benefits, U.S. companies can position themselves for success in one of the world’s most promising markets. VJM Global’s comprehensive business setup, tax planning, and compliance services ensure an efficient entry into the Indian market, tailored to your specific needs.

Now, let’s explore the key government policies that support the setup of international businesses.

India's government has introduced several initiatives to make it easier for foreign businesses, especially U.S.-based investors, to set up operations in the country. Here's a closer look at the key policies:

For U.S. businesses, these policies can significantly ease the establishment of operations and ensure long-term success in India.

Also Read: Documents Needed for Private Limited Company Registration

Having the right documents in place is essential to ensure a smooth registration process. Here’s what you’ll need to get started.

When starting a business in India as a foreign company, there are several key documents you’ll need to submit to comply with local regulations. Here’s a breakdown of the most essential documents:

When setting up a One-Person Company (OPC), the documents required are specific to this business structure:

Let’s say a U.S. investor wishes to open an OPC in India. They will also need to submit their passports, proof of address, and a lease agreement for the office space in India.

These are the key documents and steps needed to establish your business in India.

Also Read: Documents Needed For Company Registration In India From The US

With your documents in order, the next step is the registration process. Here's how to register a company in India, step by step.

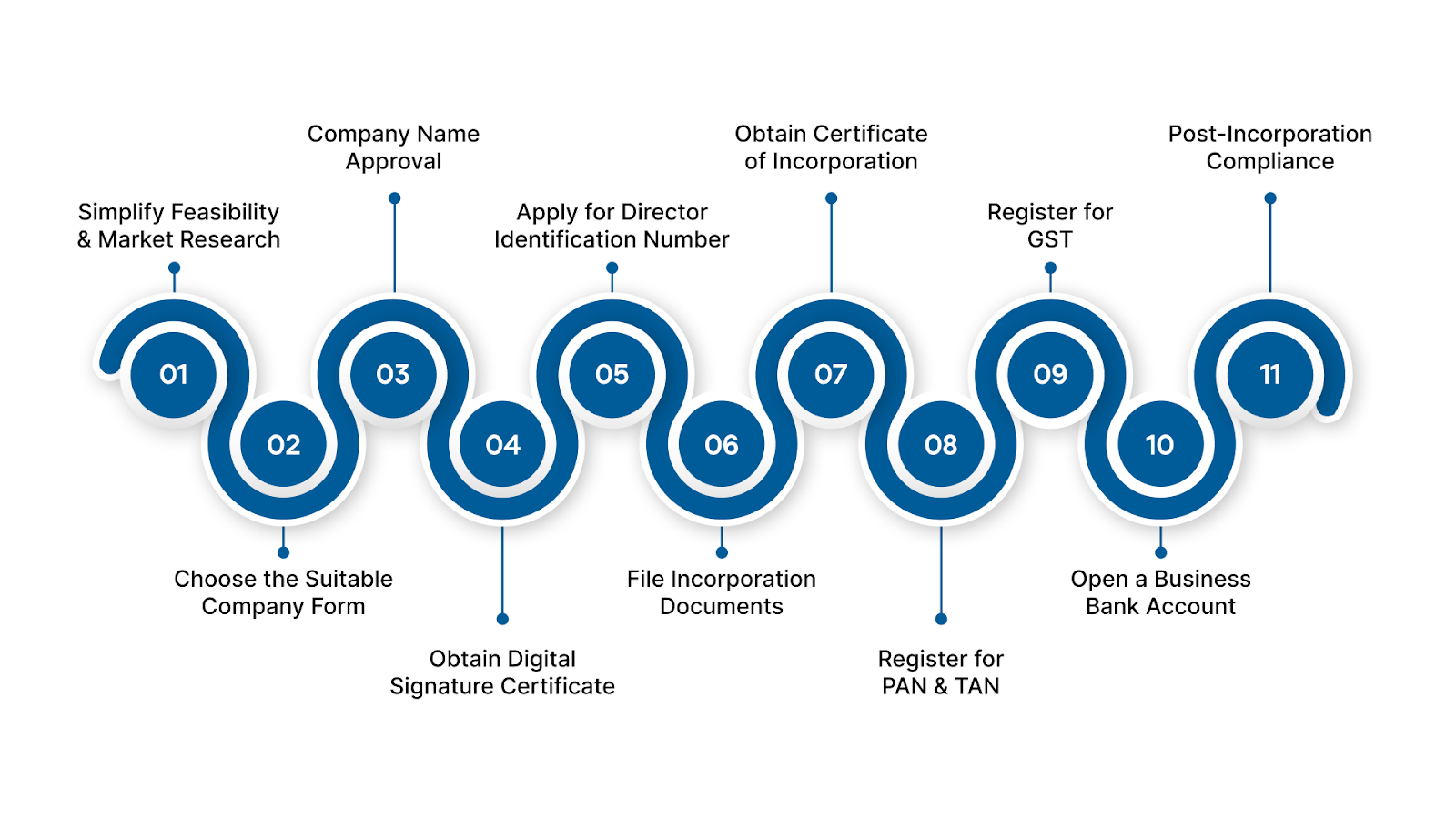

Setting up a business in India involves several steps that need to be carefully followed to ensure compliance with Indian laws. Here's a step-by-step guide to registering a company in India.

Before beginning the registration process, it's crucial to understand the Indian market. Conducting thorough market research and feasibility studies will help you assess the potential for success in India. This includes:

When choosing a business structure in India, U.S. investors must consider how each option aligns with their growth plans, risk appetite, and operational scale.

For instance, although a sole proprietorship may be the simplest option, it exposes the business owner to full personal liability, making it unsuitable for larger ventures. On the other hand, a partnership allows for shared responsibility but introduces the risk of joint liability, which can complicate decision-making in the event of disputes.

Next, select a unique name for your company. Ensure it aligns with the Ministry of Corporate Affairs (MCA) guidelines. To reserve the name:

A Digital Signature Certificate (DSC) is required for signing documents electronically. It is mandatory for all company directors and authorized signatories. Here’s how to obtain it:

Each company director needs a unique Director Identification Number (DIN). To apply:

Once the company name is approved, it’s time to file the incorporation documents. These documents are submitted via SPICe+ Part B, the company registration form.

After the registration process, the Registrar of Companies (ROC) will review your documents. Upon approval, you will receive the Certificate of Incorporation, confirming your company’s legal existence. This document includes your Corporate Identity Number (CIN).

After incorporation, you need to apply for the Permanent Account Number (PAN) and Tax Deduction and Collection Account Number (TAN), which are essential for tax-related purposes. These are often generated automatically when your company is incorporated.

If your company’s turnover exceeds the prescribed threshold or if you’re engaged in interstate trade, you need to register for Goods and Services Tax (GST). This allows you to claim input tax credits and ensures tax compliance.

To manage your finances, you will need to open a business bank account. For this, you’ll need:

After the setup, you must follow compliance regulations:

An OPC is an ideal choice for U.S. investors looking to maintain full control over their business while minimizing personal liability. To register an OPC in India, the following criteria must be met:

OPC Registration Process:

By following the steps outlined here, you can tackle the registration process and ensure your business is legally sound and ready to operate in India.

If you need expert assistance with your company setup in India, VJM Global offers end-to-end support, from registration to tax planning and compliance. Book a demo to simplify your business setup in India.

Once your company is registered, understanding the legal requirements is crucial. Let’s go over the key legal obligations for running a business in India.

When setting up a business in India, understanding the legal requirements is crucial. Here are the key legal requirements for U.S. investors:

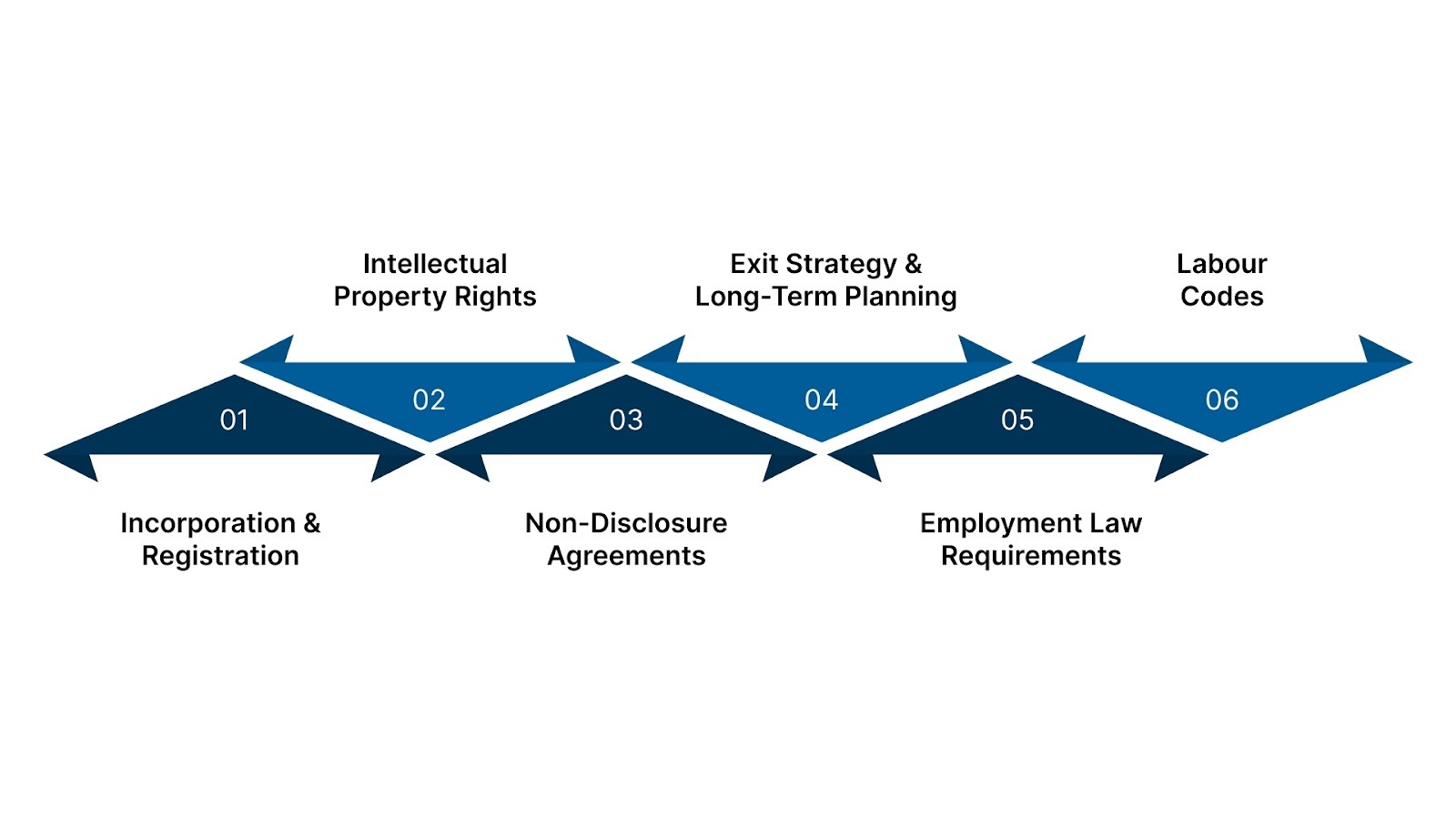

Register your business with the Ministry of Corporate Affairs (MCA) and secure a registered office in India for all official communications. This is crucial for legal recognition and ongoing operations.

Protect your business innovations by registering patents, trademarks, and copyrights. This ensures your unique products and services are safeguarded from infringement, helping maintain a competitive edge.

NDAs are essential for protecting sensitive information shared with partners, employees, and investors. These agreements ensure confidentiality and prevent unauthorized use or disclosure of business-critical data.

While growth is essential, having a clear exit strategy is equally important. Whether through mergers, acquisitions, or IPOs, planning for the future ensures smoother transitions and enables investors to realize returns when necessary.

Ensure compliance with India’s labor laws, including the Employees' Provident Funds Act, Minimum Wages Act, and Maternity Benefits Act. Also, provide clear employment contracts outlining roles, compensation, and rights for all employees.

India has consolidated 40 labor laws into four new Labour Codes. These codes simplify wage-related regulations, workplace safety, dispute resolution, and social security benefits, making it easier to navigate compliance across states.

Understanding and complying with these legal requirements helps ensure your business operates smoothly and adheres to Indian regulations.

Next, let’s break down the typical expenses you’ll incur when setting up a business in India.

Starting a business in India involves a range of costs, from government fees to professional service charges, depending on different company structures:

The exact cost of setting up a business in India will depend on the company structure, location, and whether you opt for professional assistance.

Understanding these costs upfront will help you make more informed decisions and ensure a smooth registration and compliance process.

Tackling the business setup process in India doesn’t have to be overwhelming. Here’s how VJM Global can assist you every step of the way.

Starting a business in India can be complex, but with VJM Global by your side, the process becomes clear and manageable. Here's how we can help:

With offices in multiple cities across India, VJM Global has built a reputation as a trusted partner for businesses looking to thrive in India.

Setting up a business in India offers immense potential, but it requires careful planning and an understanding of the legal, financial, and operational domains. Every step is crucial to ensuring a smooth market entry, from registering your company and understanding the associated costs to complying with tax regulations.

With the right guidance, your company can avoid common pitfalls and make informed decisions that set the stage for long-term success in India’s growing economy.

VJM Global, with its expertise in company setup, taxation, and compliance, is here to support you through each phase of this process. Our team is dedicated to simplifying the journey, whether you’re establishing a private limited company, one-person company (OPC), or any other structure.

Ready to take the next step? Contact VJM Global today, and let us help you explore the opportunities that await in the Indian market.

Yes, a U.S. citizen can start a business in India. With 100% Foreign Direct Investment (FDI) permitted in most sectors, U.S. investors can set up businesses, such as wholly owned subsidiaries or branch offices.

While not mandatory, hiring a Chartered Accountant (CA) is highly recommended. A CA can assist with filing documents, ensuring compliance, and offering business structure advice. VJM Global’s expert team provides comprehensive support, including company registration, tax planning, and compliance, to ensure a smooth setup.

To start a business in India, set clear goals, choose a compliant name, and register your company. Afterward, set up your office, hire staff, and market your business. Ensuring legal compliance is essential to avoid issues down the road.

Yes, a One-Person Company (OPC) allows a single individual to own and run a business. With limited liability and a simple compliance process, an OPC is a great option for solo entrepreneurs who want the benefits of a corporate structure without the complexity.

U.S. citizens can choose from a Private Limited Company, One-Person Company (OPC), LLP, or a Branch/Project Office. The right choice depends on ownership preferences, liability, and business goals. Each structure has unique legal and compliance requirements.