Introduction

Poor bookkeeping costs UK small businesses far more than lost receipts and messy spreadsheets. HMRC can impose penalties of up to £3,000 per failure to keep adequate records, affecting income tax returns and company tax filings. Beyond regulatory risk, inadequate financial record-keeping creates cascading problems: late payments cost the UK economy £10.7 billion annually, contributing to approximately 14,468 business closures each year. When you can't track what you're owed or what you owe, cash flow becomes guesswork rather than management.

Fixing these problems starts with understanding the full picture. This guide covers the daily mechanics of recording transactions, your legal obligations to HMRC, practical strategies to prevent compliance failures, and how to decide whether to manage bookkeeping yourself or bring in professionals.

The UK compliance landscape is demanding: Making Tax Digital mandates are expanding in phases, VAT registration triggers detailed record-keeping requirements, and HMRC's retention rules create multi-year audit exposure. Solid bookkeeping is what keeps all of that manageable.

TLDR:

- HMRC requires digital records for most businesses, with MTD for Income Tax rolling out from April 2026

- Maintain separate business accounts and keep records for 6 years (limited companies) or 5 years post-Self Assessment

- Over 1.5 million UK businesses are affected by late payments — tight invoice management is non-negotiable

- Cloud-based MTD-compatible software (Xero, QuickBooks, FreeAgent, Sage) is now effectively mandatory

- Outsource when transaction volume grows, VAT kicks in, or professional fees cost less than your time

What Is Bookkeeping (And How It Differs from Accounting)?

Bookkeeping is the day-to-day process of recording, organising, and maintaining every financial transaction your business makes — capturing sales invoices, logging purchase receipts, reconciling bank statements, and tracking VAT. The Association of Accounting Technicians defines it as "the first part of the accounting process" , focused on keeping accurate track of money flow and managing cash movements.

Accounting builds on that foundation. Bookkeeping captures the facts; accountants analyse the data bookkeepers organise, producing financial statements, forecasting future needs, planning tax strategy, and advising on business decisions. The AAT frames the distinction clearly: "Bookkeeping focuses on recording and organising financial data, while accounting is the interpretation and presentation of that data."

Understanding this split matters because it shapes the support you need as you grow:

- Bookkeeper — keeps transaction records complete and accurate, essential for correct tax returns and cash flow tracking

- Accountant — uses those records to advise on VAT registration, capital investment structure, and accounting method changes

Hiring at the wrong level costs you either strategic advice you can't yet use, or a business built on shaky financial foundations.

What Does Bookkeeping Involve for a UK Small Business?

Core Financial Records

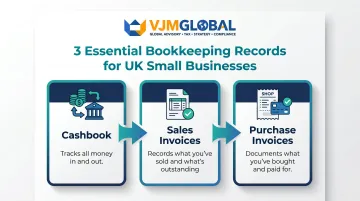

Every UK small business should maintain three foundational records:

- Cashbook — tracks all money flowing in and out of your business bank account, creating a chronological record of every transaction

- Sales invoices — records what you've sold, whether customers have paid yet, and what remains outstanding

- Purchase invoices — documents what you've bought and how it was paid for, separating paid from unpaid supplier bills

Bank reconciliation ties these together. This process matches your internal transaction records against bank statements to catch errors, duplicates, or missing entries. Reconcile weekly if you run a high-volume business, monthly at minimum.

Small discrepancies multiply quickly — a £50 mismatch in January becomes a £600 annual headache if you only reconcile at year-end.

Key Ongoing Tasks

Invoice Management

Track outgoing sales invoices with sequential numbering (INV-001, INV-002, etc.) to simplify chasing and spot gaps. File incoming purchase invoices separately: one folder for paid bills (alphabetically by supplier), another for unpaid. This structure directly supports cash flow management — you can see at a glance what you're owed and what you owe.

VAT Record-Keeping

Once you register for VAT, you must maintain detailed records of all VAT transactions:

- Input tax — VAT you pay on purchases

- Output tax — VAT you charge customers

These records support your quarterly VAT return submissions and must be kept digitally under Making Tax Digital for VAT rules. Poor VAT records create direct penalties and interest charges.

Payroll and PAYE Bookkeeping

If you employ staff, record wages, employer National Insurance contributions, and PAYE submissions accurately. Payroll errors create both financial exposure (underpayment penalties) and compliance risk with HMRC. Many small businesses outsource payroll entirely — the cost of a single HMRC correction notice typically outweighs months of outsourcing fees.

UK Legal Requirements: What HMRC Expects

Record Retention Rules

UK businesses must retain financial records for a minimum period measured from specific dates:

| Business Type | Retention Period | Measured From |

|---|---|---|

| Limited companies | At least 6 years | End of the last company financial year |

| Sole traders & partnerships | At least 5 years | After the 31 January Self Assessment deadline |

Records must be complete, accurate, and retrievable — filed away isn't enough. HMRC expects you to produce them during investigations. GOV.UK guidance notes records may need keeping longer if they show transactions covering multiple periods, or if you bought assets expected to last more than six years.

HMRC can impose penalties up to £3,000 for failure to keep or preserve adequate records — applied per tax return or per claim. First-time offenders typically receive written warnings, but repeat failures or deliberately destroyed records trigger immediate fines.

Businesses that cannot substantiate returns during compliance checks also face additional tax assessments, interest charges, and Schedule 24 inaccuracy penalties.

Making Tax Digital (MTD)

MTD for VAT has applied to all VAT-registered businesses since April 2022, requiring digital record-keeping and submission through MTD-compatible software. You cannot file VAT returns using paper records or non-compatible spreadsheets.

MTD for Income Tax Self Assessment rolls out in three phases for sole traders and landlords:

| Phase | Qualifying Income Threshold | Start Date | Applies to Tax Year |

|---|---|---|---|

| 1 | Over £50,000 | 6 April 2026 | 2024-25 |

| 2 | Over £30,000 | 6 April 2027 | 2025-26 |

| 3 | Over £20,000 | 6 April 2028 | 2026-27 |

Qualifying income combines gross income from self-employment and property. If your combined income exceeds the threshold, you must use MTD-compatible software to maintain digital records and submit quarterly updates to HMRC. First-time filers are exempt until after submitting their first Self Assessment.

Setting up compliant digital systems now — even before the threshold applies to you — avoids painful transitions later. HMRC research found 67% of businesses using MTD-compatible software reported fewer mistakes, and 80% found the process easy. Starting early also gives you time to choose the right software and iron out any data migration issues before deadlines arrive.

MTD shapes how you handle VAT and Self Assessment too — both of which carry their own record-keeping requirements.

VAT and Self Assessment Obligations

You must register for VAT if your total taxable turnover for the last 12 months exceeds £90,000 (increased from £85,000 in April 2024). VAT registration triggers detailed record-keeping requirements: track input and output VAT separately, submit returns quarterly, and maintain digital records under MTD. The VAT Cash Accounting Scheme is available to businesses with estimated VAT taxable turnover of £1.35 million or less, allowing you to account for VAT when payment is received rather than when invoiced.

From the 2024-25 tax year, cash basis became the default accounting method for sole traders and partnerships, with the previous £150,000 turnover cap removed. You now record income when received and expenses when paid, simplifying bookkeeping for most small businesses. If you prefer traditional accrual accounting (recording when invoiced rather than when paid), you must opt out explicitly. Limited companies cannot use cash basis.

The method you choose — cash basis or accruals — directly affects what gets recorded and when. Switching mid-year without proper adjustments can produce duplicate income entries or missed deductions, which creates exactly the kind of discrepancy that triggers a compliance check.

Best Practices and Tips for UK Small Business Bookkeeping

Build the Right Habits

Separate Business and Personal Finances

Open a dedicated business bank account from day one and use it exclusively for business transactions. Mixing finances is the most common — and most costly — mistake small business owners make. The consequences are practical:

- Renders tax calculations inaccurate and unreliable

- Creates legal exposure for sole traders and directors

- Makes bank reconciliation nearly impossible

- Requires individual explanations for every personal transaction during HMRC investigations

Set a Consistent Bookkeeping Schedule

Consistency matters more than frequency. High-transaction businesses (retail, hospitality) should reconcile daily. Most service businesses manage well with weekly updates. Monthly is the absolute minimum. Treat your bookkeeping schedule as non-negotiable — catching errors quickly means small corrections rather than reconstructing months of data under deadline pressure.

Track and Categorise All Business Expenses

Keep receipts (digital or physical) for every claim. HMRC accepts scanned receipts and photos, so use receipt-scanning apps if paper overwhelms you. Categorise expenses consistently using HMRC's recognised categories:

- Office costs (stationery, phone bills)

- Travel costs (fuel, parking, train fares)

- Staff costs (salaries, subcontractors)

- Premises costs (heating, business rates)

- Financial costs (insurance, bank charges)

- Marketing (website costs, advertising)

Allowable expenses reduce taxable profit directly — poor expense tracking costs you money at tax time. Under cash basis accounting, all items bought and kept for the business (except cars) are claimed as expenses immediately, simplifying the process further.

Stay on Top of Reporting and Compliance

Produce Monthly Management Reports

At minimum, generate a profit and loss statement and balance sheet each month. Monthly reporting reveals whether you're actually profitable, flags cash flow pressure points early, and removes the year-end panic of reconstructing financial history. These reports should take under an hour to produce if your bookkeeping is current.

Practise Strict Credit Control

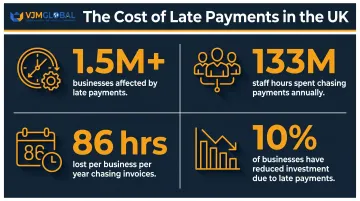

Number sales invoices sequentially, set clear payment terms (for example, "Payment due within 14 days"), and implement a process for chasing overdue invoices. Late payments are a leading cause of cash flow problems. Government research puts the scale in sharp relief:

- Over 1.5 million UK businesses are affected by late payments

- Businesses spend an estimated 133 million staff hours annually chasing them

- The average business loses 86 hours per year to payment follow-up

- 10% of affected businesses have reduced investment as a direct result

Small businesses were paid an average of 8.2 days late according to Xero's UK data. Tight invoice management — prompt issuing, clear terms, and systematic chasing — directly protects your working capital.

Choosing the Right Bookkeeping Software

Select software based on five criteria:

MTD Compatibility: Essential for VAT-registered businesses and increasingly important for sole traders approaching the Income Tax thresholds. Check HMRC's official software directory to verify compatibility.

Ease of Use: Software you find frustrating won't get used consistently. Most platforms offer free trials — test the interface before committing.

Bank Feeds and Automation: Cloud software with open banking integration downloads transactions automatically and suggests categorisations, reducing manual data entry by 60-80%.

Integrations: Consider whether the software connects to tools you already use: payroll systems, e-commerce platforms, CRM software, or payment processors.

Scalability: Adding employees, VAT registration, or multi-currency trading shouldn't force a platform switch later.

The most widely used cloud platforms in the UK are:

- Xero — comprehensive features, strong third-party integrations, suits growing SMEs with complex needs

- QuickBooks — user-friendly interface, extensive app marketplace, popular with service businesses

- FreeAgent — free for NatWest, Royal Bank of Scotland, and Ulster Bank business account holders (note: HSBC is not included); designed for freelancers and micro-businesses

- Sage — established brand with both cloud and desktop options, strong payroll integration

All four are MTD-recognised by HMRC. The best choice depends on transaction volume, whether you have employees, and VAT registration status. Don't choose based on features alone — consider the total cost including add-ons, training time, and whether your accountant or bookkeeper already works with that platform.

That last point matters more than most small business owners realise. If your accountant already uses Xero or QuickBooks, onboarding is faster and collaboration is seamless — you both work from the same live data rather than emailing spreadsheets back and forth.

Cloud-based software also has clear advantages over desktop options:

- Real-time access from any device or location

- Automatic bank reconciliation via open banking feeds

- Shared live data with your bookkeeper or accountant — no version-control issues

- No manual file transfers or software update headaches

DIY vs. Outsourced Bookkeeping: Making the Right Call

DIY bookkeeping makes sense in limited circumstances:

- You're early-stage with fewer than 50 transactions per month

- You have a financial or accounting background

- The time investment won't cut into revenue-generating work

Even then, use proper software from day one. Spreadsheets create compliance risk and don't scale.

Clear signals indicate it's time to outsource:

- Transaction volume is growing beyond weekly management

- You've hired employees and run payroll

- VAT registration has triggered MTD obligations

- You're spending 5+ hours weekly on bookkeeping that could be spent on sales, delivery, or strategy

- You've missed deadlines or received HMRC correspondence about incomplete records

Calculate the opportunity cost: if your time is worth £50-£100 per hour and you spend 6 hours monthly on bookkeeping, that's £300-£600 in lost productive time. Professional bookkeeping for a small business typically costs £150-£400 monthly — often a net saving once you account for redirected time and avoided compliance errors.

Outsourced bookkeeping for UK small businesses typically includes:

- Daily or weekly transaction recording and categorisation

- Bank reconciliation

- Invoice management (sales and purchases)

- VAT return preparation and submission

- Payroll processing and PAYE filings

- Monthly management reports (P&L, balance sheet)

- Year-end accounts preparation support

When choosing a provider, look for:

- UK compliance expertise covering HMRC rules, MTD, and VAT

- Integration with your existing software

- Regular reporting cadence (monthly at minimum)

- Transparent, fixed-fee pricing

- Qualifications from the Institute of Certified Bookkeepers (ICB) or Association of Accounting Technicians (AAT)

- AML supervision registration — either through a professional body or directly with HMRC

VJM Global has supported 250+ UK businesses with outsourced bookkeeping, providing dedicated financial professionals and full compliance support across HMRC requirements and MTD obligations.

Frequently Asked Questions

Frequently Asked Questions

Is bookkeeping in demand in the UK?

Yes. The UK bookkeeping industry has grown at a compound annual rate of 1.7% between 2020 and 2025. Demand is driven by Making Tax Digital expansion, growing SME numbers, and increasing compliance complexity, making skilled bookkeepers and outsourced services consistently sought after.

Do you need a licence to be a bookkeeper in the UK?

No specific licence is legally required, though most professional bookkeepers hold qualifications from ICB or AAT. Anyone providing bookkeeping, tax advice, or accounts preparation services must register for anti-money laundering supervision — either through a recognised professional body or directly with HMRC.

What records do small businesses need to keep for HMRC?

Core records to retain:

- Bank statements and sales/purchase invoices

- Expense receipts and payroll records

- VAT records (if registered) and previous tax returns

Retention periods: 6 years for limited companies; 5 years after the 31 January Self Assessment deadline for sole traders.

What is the difference between bookkeeping and accounting?

Bookkeeping is the day-to-day recording and organisation of financial transactions. Accounting is the broader discipline of interpreting that data to produce financial statements, plan tax strategy, and support business decisions. Bookkeeping feeds into accounting.

What bookkeeping software do UK small businesses use?

The most popular MTD-compatible options are Xero, QuickBooks, FreeAgent, and Sage. The best choice depends on transaction volume, complexity, employee count, and VAT registration status. FreeAgent is free for NatWest, Royal Bank of Scotland, and Ulster Bank business account holders.

When should a small business outsource its bookkeeping?

Outsourcing typically makes sense when transaction volume grows beyond weekly management, payroll or VAT obligations are added, or your time is better spent on revenue-generating work. In most cases, the fee pays for itself through time saved and errors avoided.